Go to IRS.gov/Account to securely access information about your federal tax account. Go to IRS.gov/SocialMedia to see the various social media tools the IRS uses to share the latest information on tax changes, scam alerts, initiatives, products, and services. Don’t post your social security number (SSN) or other confidential information on social media sites. Always protect your identity when using any social networking site.

- However, do not increase your basis for depreciation not allowed for periods during which either of the following situations applies.

- We follow strict ethical journalism practices, which includes presenting unbiased information and citing reliable, attributed resources.

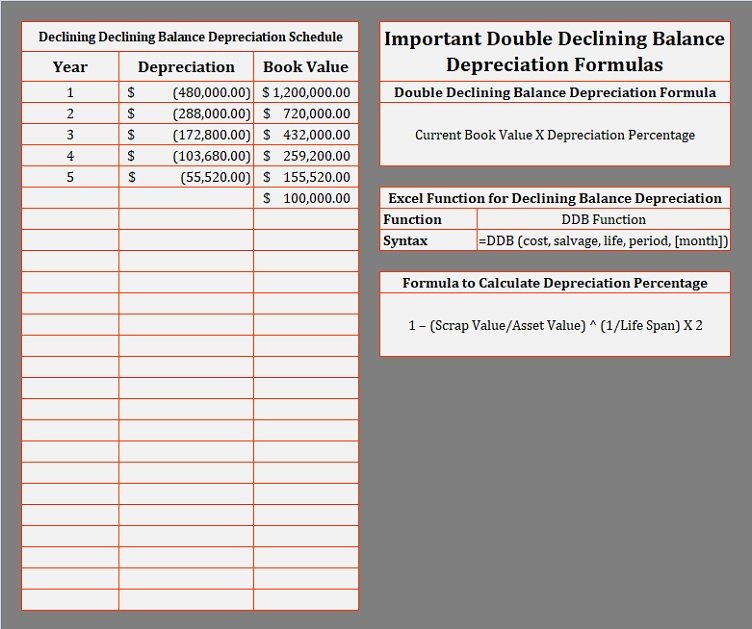

- To calculate the depreciation rate for the DDB method, typically, you double the straight-line depreciation rate.

- The partnership’s taxable income from the active conduct of all its trades or businesses for the year was $1,110,000, so it can deduct the full $1,110,000.

What Does the Declining Balance Method Tell You?

In figuring the taxable income of an S corporation, disregard any limits on the amount of an S corporation item that must be taken into account when figuring a shareholder’s taxable income. On February 1, 2023, the XYZ Corporation purchased and placed in service qualifying section 179 property that cost $1,160,000. It elects to expense the entire $1,160,000 cost under section 179. In June, the corporation gave a charitable contribution of $10,000. A corporation’s limit on charitable contributions is figured after subtracting any section 179 deduction. The business income limit for the section 179 deduction is figured after subtracting any allowable charitable contributions.

What Assets Are DDB Best Used For?

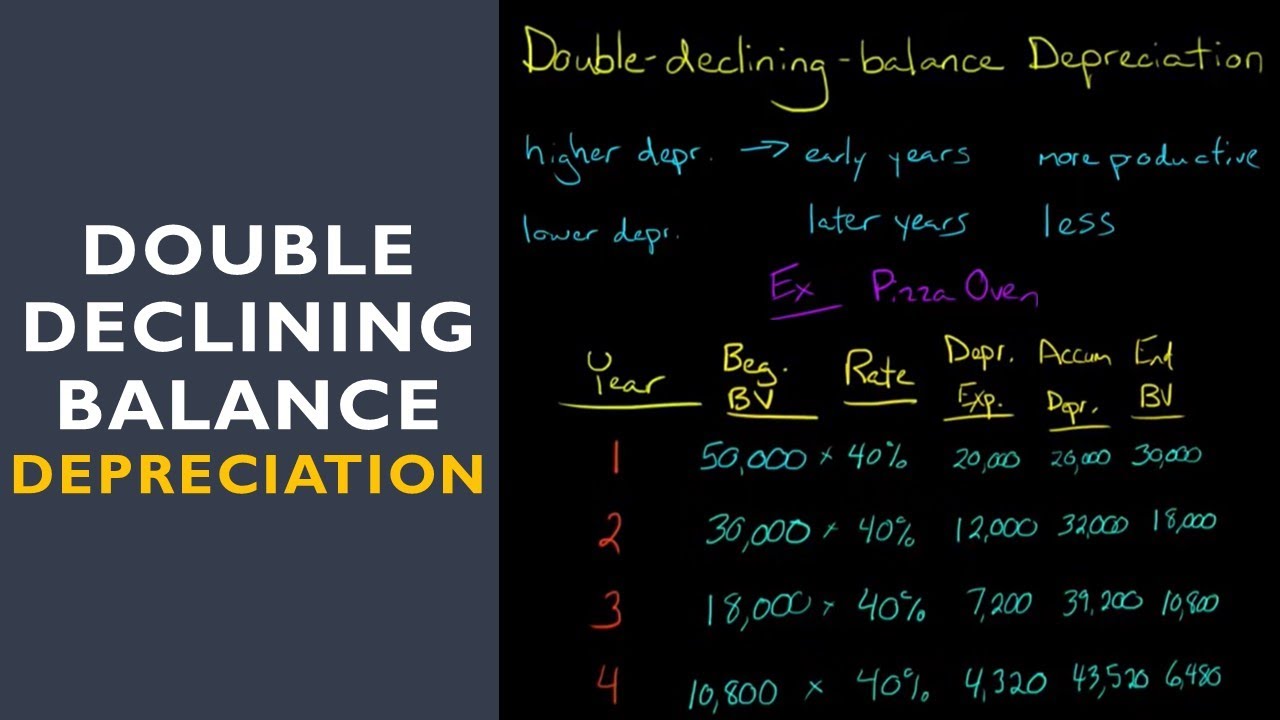

You should consult your own legal, tax or accounting advisors before engaging in any transaction. The content on this website is provided “as is;” no representations are made that the content is error-free. Now that we have a beginning value and DDB rate, we can fill up the 2022 depreciation expense column. The diagram below shows the analysis by year of the declining method depreciation expense. Note that the depreciation in the fifth and final year is only for $1,480, rather than the $3,240 that would be indicated by the 40% depreciation rate.

AccountingTools

Even if the requirements explained in the preceding discussions are met, you cannot depreciate the following property. Generally, containers for the products you sell are part of inventory and you cannot depreciate them. However, you can depreciate containers used to ship your products if they have a life longer than 1 year and meet the following requirements. You made a down payment to purchase rental property and assumed the previous owner’s mortgage.

After the dollar limit (reduced for any nonpartnership section 179 costs over $2,890,000) is applied, any remaining cost of the partnership and nonpartnership section 179 property is subject to the business income limit. In general, figure taxable income for this purpose by totaling the net income and losses from all trades and businesses you actively conducted during the year. Net income or loss from a trade or business includes the following items. This chapter explains what property does and does not qualify for the section 179 deduction, what limits apply to the deduction (including special rules for partnerships and corporations), and how to elect it. Several years ago, Nia paid $160,000 to have a home built on a lot that cost $25,000. Before changing the property to rental use last year, Nia paid $20,000 for permanent improvements to the house and claimed a $2,000 casualty loss deduction for damage to the house.

For certain specified plants bearing fruits and nuts planted or grafted after December 31, 2023, and before January 1, 2025, you can elect to claim a 60% special depreciation allowance. To be qualified property, long production period property must meet the following requirements. In addition, figure taxable income without regard to any of the following. If you and your spouse elect to amend your separate returns by filing a joint return after the due date for filing your return, the dollar limit on the joint return is the lesser of the following amounts.

A term interest in property means a life interest in property, an interest in property for a term of years, or an income interest in a trust. If Maple buys cars at wholesale prices, leases them for a short time, and then sells them at retail prices or in sales in which a dealer’s profit is intended, construction equipment financing and leasing the cars are treated as inventory and are not depreciable property. In this situation, the cars are held primarily for sale to customers in the ordinary course of business. Accruing tax liabilities in accounting involves recognizing and recording taxes that a company owes but has not yet paid.

GAAP guidelines highlight several separate, allowable methods of depreciation that accounting professionals may use. Because the double-declining balance method results in larger depreciation expenses near the beginning of an asset’s life—and smaller depreciation expenses later on—it makes sense to use this method with assets that lose value quickly. The declining balance method is one of the two accelerated depreciation methods and it uses a depreciation rate that is some multiple of the straight-line method rate. The double-declining balance (DDB) method is a type of declining balance method that instead uses double the normal depreciation rate. An asset costing $20,000 has estimated useful life of 5 years and salvage value of $4,500.