Sales will closewith the temporary credit balance accounts to Income Summary. On January 2, FitTees purchased 2,000 units of designer shirts from a new supplier, FRESH Distributors, Inc. for cash worth at $28 per unit. On January 2, FitTees purchased 2,000 units of designer shirts from a new supplier, FRESH Distributors, Inc. for cash at $28 per unit.

Periodic versus Perpetual Inventory Systems

The perpetual system aligns closely with the accrual basis of accounting, where transactions are recorded when they occur. In contrast, the periodic system is akin to the cash basis of accounting, recognizing transactions when the cash is exchanged. track your charitable donations to save you money at tax time This distinction can influence the timing of expense recognition and, consequently, the business’s reported profitability within a given period. The advantage of a perpetual system in providing a rolling estimate of COGS is clear.

The difference between perpetual LIFO and periodic LIFO

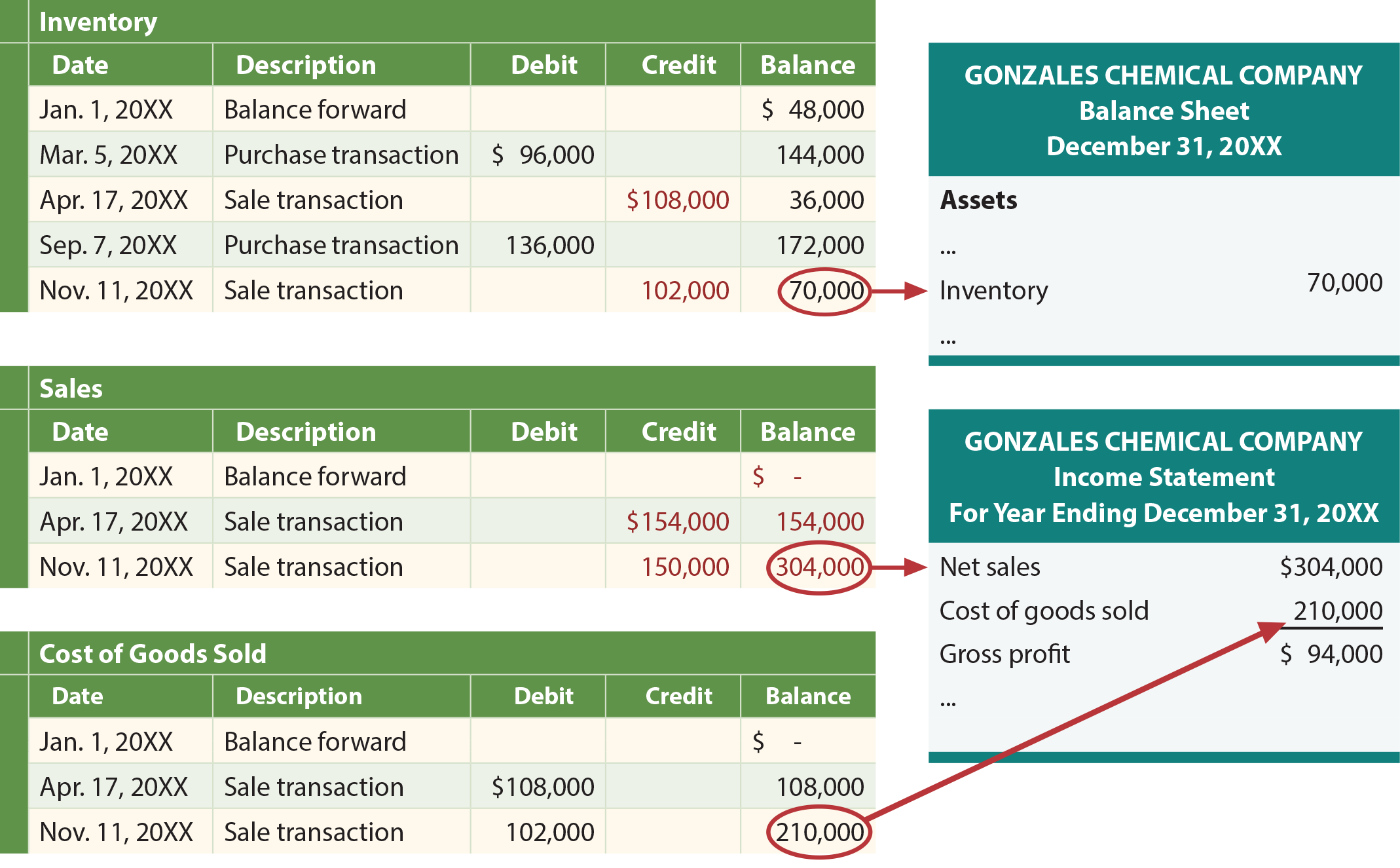

Inventory management formulas can tell you when to order more inventory, how much to order, the lead time needed before placing an order and how much stock you require to keep in safety. The following table, ledgers, and financial statements reveal the application of perpetual LIFO. The journal entries are not repeated here but would be the same as with FIFO; only the amounts would change. Not only must an adjustment to Merchandise Inventory occur atthe end of a period, but closure of temporary merchandisingaccounts to prepare them for the next period is required. Temporaryaccounts requiring closure are Sales, Sales Discounts, SalesReturns and Allowances, and Cost of Goods Sold.

- The update and recognition could occur at the endof the month, quarter, and year.

- On January 2, FitTees purchased 2,000 units of designer shirts from a new supplier, FRESH Distributors, Inc. for cash at $28 per unit.

- The scan triggers the inventory management system to automatically deduct the purchased units and update them as needed and will constantly track the stock level of each product.

- However, the impact is only indirect because the number is simply carried over from the previous period.

The Cost of Goods Sold (COGS)

Periodic systems are more suitable for businesses not affected by slow inventory updates. These include emerging businesses, ones that offer services or companies that have low sales volume and easy-to-track inventory. Companies whose staff struggle with a perpetual system, for instance those with seasonal help, would also benefit from maintaining a periodic system.

So, under the perpetual inventory method, we calculated COGS for the period of $99,100—but we didn’t know that exact amount until we took a physical count. In this final approach to maintaining and reporting inventory, each time that a company buys inventory at a new price, the average cost is recalculated. Therefore, a moving average system must be programmed to update the average whenever additional merchandise is acquired. The ability to estimate COGS continuously also provides a company using a perpetual inventory system the ability to estimate gross profit continuously.

Thisexample assumes that the merchandise inventory is overstated in theaccounting records and needs to be adjusted downward to reflect theactual value on hand. Square accepts many payment typesand updates accounting records every time a sale occurs through acloud-based application. This enhanced product allowsbusinesses to connect sales and inventory costs immediately. Abusiness can easily create purchase orders, develop reports forcost of goods sold, manage inventory stock, and update discounts,returns, and allowances. With this application, customers havepayment flexibility, and businesses can make present decisions topositively affect growth. Perpetual inventory and periodic inventory are both accounting methods used by businesses to track the number of products they have available.

The time commitment to train andretrain staff to update inventory is considerable. In addition,since there are fewer physical counts of inventory, the figuresrecorded in the system may be drastically different from inventorylevels in the actual warehouse. A company may not have correctinventory stock and could make financial decisions based onincorrect data. Inventory management plays a pivotal role in financial reporting, as inventory is a significant asset that impacts both the balance sheet and the income statement. Accurate inventory records are essential for reliable financial statements, which in turn are crucial for investors, creditors, and other stakeholders who rely on this information to make informed decisions. The valuation of inventory—whether by FIFO (First-In, First-Out), LIFO (Last-In, First-Out), or weighted average cost—can affect the cost of goods sold and, consequently, the gross profit reported.

Relying on data provided by electronic point-of-sale technology, it provides a highly detailed view of changes in inventory and immediate reporting on the amount of inventory in stock. Perpetual inventory systems differ from periodic inventory systems, in which a company must instead depend on regularly scheduled physical counts. The perpetual inventory system gives real-time updates and keepsa constant flow of inventory information available fordecision-makers. With advancements in point-of-sale technologies,inventory is updated automatically and transferred into thecompany’s accounting system. This allows managers to make decisionsas it relates to inventory purchases, stocking, and sales.